This section provides an overview of our research process. Our Terms of Service, relevant disclosures, and other legal notices can be found here.

Frequently Asked Questions:

How does Disclosure Insight® / Probes Reporter® Know a Public Company has an Undisclosed SEC Investigation?

What Happens After You Get an Early Indication of an SEC Investigation?

Your Favorite Company May Have an Undisclosed SEC Probe. Now What?

When we report on risk of undisclosed SEC investigative activity for a company, it is based upon a response from the United States Securities and Exchange Commission (SEC) to one of the approximately 2,500 Freedom of Information Act (FOIA) requests we file with the agency each year.

Our requests seek certain information on public companies. Our reporting of undisclosed SEC investigative risk starts with the SEC’s assertion of a law enforcement exemption in response to one of our FOIA requests.

Note: In our research notes and reports, our use of the term "Early Signal" or "Confirmed" SEC investigation pertains to technicalities related to the FOIA. For risk assessment purposes, we treat them as essentially the same. This write-up assumes as much as well.

Background on the Law Enforcement Exemption

According to FOIA.gov, exemptions to the FOIA can be best understood as follows,

"Not all records can be released under the FOIA. Congress established certain categories of information that are not required to be released in response to a FOIA request because release would be harmful to governmental or private interests. These categories are called 'exemptions' from disclosures. Still, even if an exemption applies, agencies may use their discretion to release information when there is no foreseeable harm in doing so and disclosure is not otherwise prohibited by law. There are nine categories of exempt information ..."

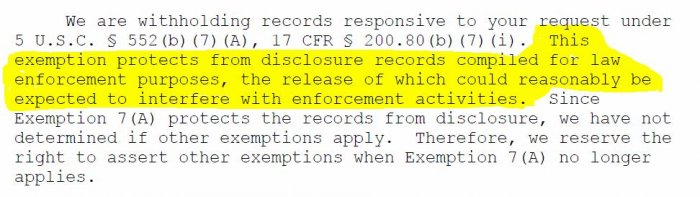

Exemption (b)(7)(A) is an element of the law enforcement exemption of the FOIA, and is basically the government's way of saying that, "we can't tell you what we are investigating, because the investigation is ongoing."

Below you can see an excerpt of a real letter sent to us from the FOIA office of the SEC in which the government cited Exemption (b)(7)(A) as means to block our access to records. We encounter this language many times --

When we receive such a response from the FOIA office we automatically file an administrative appeal with the Office of the General Counsel of the SEC. This allows a different set of eyes to review our original request.

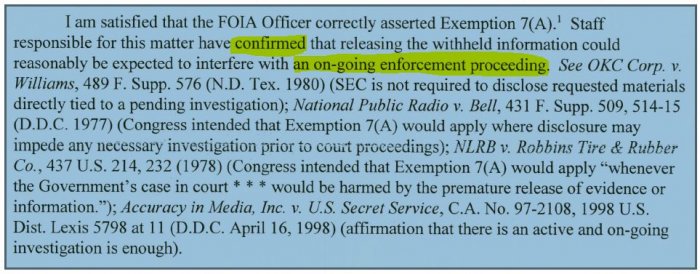

Sometimes the appeal response will tell us the investigation is over and our request has been remanded for further processing. On rare occasion the appeal response can tell us an error was made in the original response sent by the FOIA office. More commonly, the appeal response will affirm the initial denial made by the FOIA office. The letter excerpt below shows language we typically see when the SEC does this --

Helpful Background on SEC Investigations

An SEC investigation is a fact-finding inquiry. There is no denying that those words, "probe", "inquiry", "document request", and/or "investigation” can have implications that can be quite serious. Therefore, it is important for us to offer as balanced a perspective as possible on this topic, both for our readers and the public companies on which we obtain information.

The implications of any SEC investigation, whether disclosed or not, can be quite serious. That's the first thing you need to know. The proverbial cops have shown up and they have a bunch of questions. Any lawyer in the land will advise that poses inherent danger, even to the innocent. Having said that, it could also mean very little. (BTW, we are not attorneys here at Probes Reporter but we rely heavily on them for advice.)

The mere existence of an SEC investigation does not necessarily mean that anybody has done anything wrong. Indeed when the SEC sends out a request for information in an investigation it advises the recipient of the request that an investigation does not mean that anyone has broken the law or that the SEC has a negative opinion of any person, entity or security.

The FOIA office of the SEC reminds us of the same when they block our access to records on a company over concerns their release could potentially interfere with law enforcement activities. Below is language typically included by the SEC in those same letters to us --

Although SEC proceedings are civil proceedings, not criminal actions, the consequences of SEC enforcement actions can be quite severe. Among other things, the SEC can seek and obtain substantial fines, force companies to restate their financial statements and to change their accounting practices in significant ways. The SEC can also seek to bar persons from serving as officers or directors of public companies and thus can have a serious impact on a company's management. In extreme cases, the SEC can also refer a matter to the Department of Justice for criminal prosecution.

The SEC is an independent regulatory agency that was created by the Securities Exchange Act of 1934. The SEC is empowered to conduct investigations to determine whether any person or entity is violating or has violated the federal securities laws. SEC investigations are initially private and nonpublic, although sometimes a company subject to an investigation will voluntarily disclose it.

The SEC conducts investigations in two ways, formally and informally.

The arm of the SEC that conducts investigations is its Enforcement Division in Washington, DC and its counterparts in the SEC's regional offices spread throughout the country. This is often confused with the SEC's Corporation Finance Division which conducts the reviews and sends out so-called "comment letters".

A formal investigation is one where the SEC uses its subpoena power to compel the production of documents and witnesses. An informal investigation relies on the cooperation of the persons from whom information is sought.

Whether an investigation is described as formal or informal, the implications may be serious.

Both kinds of investigations can lead to so-called "enforcement proceedings." Both kinds of investigations can also lead to no action at all.

Frequently, companies engaged in these matters will tell investors they are involved in an “informal inquiry”, thus giving the impression it's not that big of a deal. Some will simply disclose receipt of a "document request" from the SEC. That too is likely an investigation in disguise. Guard against the desire to take comfort in these words.

It's worth noting that the SEC's investigation of Tyco more than a decade ago, which ultimately led to prison sentences for senior executives of the company, is believed to have never gone beyond the informal stage.

The status of SEC investigations changes all the time.

Those with an interest in a company exposed to an SEC probe are advised that silence does not necessarily mean absence of risk. You can't rely on a disclosure made a year ago either. Conversations take place, documents are produced, and testimony is requested and given. Matters that start out as informal inquiries can easily become formal without the company ever disclosing as much.

The SEC often shares the information it obtains in its investigations with other federal and state law enforcement agencies, including the FBI, the Department of Justice, and the IRS, just to name a few. The Department of Justice and the US Attorneys located throughout the country sometimes work closely with the SEC and, based on what they learn, criminal prosecutions can result. As an example, Foreign Corrupt Practices Act investigations are routinely coordinated between the SEC and Justice.

SEC Investigations are not the same as "Comment Letters"

Again, the arm of the SEC that conducts investigations is its Enforcement Division. This is often confused with the SEC's Corporation Finance Division which conducts the reviews and sends out so-called "comment letters".

Sarbanes-Oxley requires that every public company be reviewed at least once every three years. These reviews often involve the exchange of comment letters with the registrant. The following is from SEC.gov explaining the role the Corporation Finance Division's review and comment letter process --

Through the Division’s filing review process, we selectively review filings made under the Securities Act of 1933 and Securities Exchange Act of 1934 both to monitor and to enhance compliance with disclosure and accounting requirements. The Division concentrates its review resources on disclosures that appear to be inconsistent with Commission rules or applicable accounting standards, or that appear to be materially deficient in their rationale or in clarity.

In the course of a review, the staff may issue comments to a company to elicit better compliance with applicable disclosure requirements. In response to those comments, a company may revise its financial statements or amend its disclosure to provide additional or enhanced information, or may undertake to revise its financial statements or other disclosures in future filings. This comment process deters fraud and facilitates investor access to information necessary to make informed investment decisions, thus enhancing the efficiency of the capital markets. Where appropriate, the Division refers matters to the Division of Enforcement.

Often, investors will confuse a company's disclosure of a "document request" with the comment letter process. More often than not, we've found companies disclosing these "document requests" are really making a stealth disclosure of an SEC investigation.

It's also worth noting that while every public company gets reviewed, not every public company gets a comment letter from the SEC when it is reviewed. They are sent only when deemed necessary.

Our History with SEC Investigative Records:

FOIA as a lawful way to warn investors about undisclosed SEC investigations, you can imagine some were not happy with us.

Starting in early 2002, the SEC started to act in a way that we judged to be in violation of the Freedom of Information Act. As a result, we filed litigation against the SEC in the US District Court, District of Minnesota on October 18, 2004 to compel compliance with the FOIA (Gavin v. SEC, No. 04-4522).

Largely as a result of that litigation, we remain able to lawfully bring you timely warnings of undisclosed SEC investigative activity.

—Disclosure Insight®

© 2012-2024, Disclosure Insight, Inc. and Probes Reporter, LLC. All rights reserved.

Copyright Warning and Notice

The works of authorship contained in the accompanying material, including but not limited to all data, design, text, images, charts and other data compilations or collective works are owned by Probes Reporter, LLC or one of its affiliates and may not be copied, reproduced, transmitted, displayed, performed, distributed, rented, sublicensed, altered, or stored for subsequent use, in whole or in part in any manner, without the prior written consent of Probes Reporter, LLC.

Photocopying or electronic distribution of any of the accompanying material or contents without the prior written consent of Probes Reporter, LLC violates U.S. copyright law, and may be punishable by statutory damages of up to $150,000 per infringement, plus attorneys’ fees (17 USC 504 et. seq.). Without advance permission, illegal copying includes regular photocopying, faxing, excerpting, forwarding electronically, and sharing of online access.