Disclosure Insight®, formerly known as Probes Reporter®, is an independent publisher of investment research focused on public company interactions with the Securities and Exchange Commission (SEC).

Our Editorial Mission

- Alert you to public companies with undisclosed SEC probes.

- Provide records & analysis on closed SEC probes.

- Help interpret disclosed SEC investigative activity.

- Predict those companies whose conduct, transactions, or disclosures may subject them to an SEC investigation.

Why it Matters

More often than not, we find public companies either do not disclose their SEC probes, or, when they do disclose, they rarely provide enough information for investors to meaningfully analyze the risk it poses.

An SEC investigation, whether or not it is disclosed, holds the potential to destabilize a company, distract its management, and/or interfere with underlying fundamentals. This impact can last long after an SEC investigation has ended, even when no enforcement action was formally taken (as happens with most SEC probes).

Our goal is to obtain SEC investigative records on public companies so you can assess that risk on your own. To help you do that, each year we file about 2,500 Freedom of Information Act (“FOIA”) requests and hundreds of administrative appeals with the SEC and, sometimes, other agencies. We’ve been doing this since the year 2000.

Our SEC Investigation Update reports summarize the responses we received to our FOIA requests on a company, including documents the SEC released on closed investigations. Our Disclosure Insight® reports typically provide more in-depth commentary and analysis on public company interactions with investors and with the SEC.

You can take comfort in knowing that FOIA requests and appeals cited in any of our reports are 100% the result of our own work product.

Responses we receive are in black and white, on government letterhead. The paper trail is fully documented.

Our reports otherwise take no view on a public company’s fundamental outlook or whether you should buy, sell, or hold its securities.

As it's been since our start in 2000, we never once shorted the company's we write on. Our sole source of revenue is client subscriptions.

History of Disclosure Insight

Disclosure Insight, based in Minnesota, was founded by John P. Gavin, CFA. Mr. Gavin is a holder of the right to use the Chartered Financial Analyst® designation. He has over 35 years of experience as a professional investor & entrepreneur.

Disclosure Insight's origins date back to 2000, when Mr. Gavin started SEC Insight/Disclosure Insight.

![]()

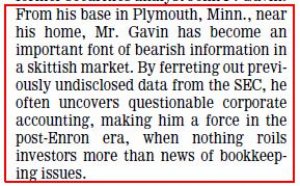

Since the late 90’s, Mr. Gavin has been steadily filing FOIA requests, primarily with the US Securities and Exchange Commission. These requests primarily seek records pertaining to investigations the SEC and other agencies conduct on publicly-traded companies. Responses received and records released in response to these FOIA requests may then be incorporated into research reports published and disseminated to the investing public by Disclosure Insight, Inc.

Highlights of his Mr. Gavin’s FOIA work include the fact that SEC comment letters that once required a FOIA request to obtain, are now routinely posted by the SEC on the internet for free. He also brought litigation against the SEC in 2004 for previous failures to comply with the FOIA. His litigation succeeded in stopping the SEC from using the “refuse to confirm or deny” response as final answer on his requests, also known as the Glomar response.

Mr. Gavin’s FOIA efforts have been covered in mainstream media including the New York Times, Wall Street Journal, and The Economist. He regularly appears in television and radio interviews as well as online media outlets to comment on the SEC and public company disclosure practices.

Our Editorial Approach

As an independent investment research and information provider, at Disclosure Insight we take our role in capital markets very seriously. Producing the kind of reports and analysis that people can rely on informs our analytical and editorial approach to all of our work here. We are the first to say we can't guarantee to always get it right. But we do our very best.

Beholden to no one, we follow the facts where they lead us, without fear or favor. We are indifferent to what a company makes, sells, does, or who is running it. Whether all the mutual funds or Wall Street analysts "love" a company, or all the hedge funds "hate" it means nothing to us. No one can pay us to write about a company or to change what our findings disclose.

If we say it is a fact we will cite our sources. For example, if we tell you a company has an undisclosed SEC investigation, it's because our source data for such a claim starts with a thoroughly documented paper trail. We have a copy of our original FOIA request as written and submitted to the SEC by us. In response, we have a genuine document, addressed only to us, in our possession, in black & white, and on government letterhead.

If we express any assumptions, interpretations, speculation, and/or opinions we will strive to be clear in identifying them as such. On those rare occasions when mistakes do occur, we strive to correct them as quickly as possible.

Disclosure Insight, Inc. requires its employees and principals to adhere to the CFA Institute Code of Ethics and Standards of Professional Conduct regarding potential conflicts of interest (see more below).

Dealing with Errors

Despite our outstanding track record, we want to be clear on one thing; like any enterprise run by human beings, we can't catch everything and we don't pretend that we can. The official government documents and company filings upon which we rely can contain errors. Fortunately, our experience shows these kinds of errors are truly rare. But they happen.

In those rare instances when errors have occurred, we issued a correction and/or clarification as quickly as possible. You can expect the same standard of editorial excellence from us today. We'd rather take the short-term heat that comes from making - and owning - an honest mistake than the long-term damage to reputation that comes about when mistakes are not owned.

Potential Conflicts of Interest

A common question that arises is whether we try to make money from trading in the securities of those public companies we write about. In short, the answer is '"No. Not ever. Period."

Disclosure Insight, Inc. requires its employees and principals to adhere to the CFA Institute Code of Ethics and Standards of Professional Conduct regarding potential conflicts of interest. This includes prohibiting its employees and principals from trading in their own accounts in any manner which might be deemed in conflict with our readers, whether paying subscribers or not.

Disclosure Insight, Inc. prohibits its employees and principals from trading of any kind in any individual public company security (or derivative thereof), of any company on which we have received a response from the United States Securities and Exchange Commission (or other regulatory authority) to one of our Freedom of Information Act (FOIA) requests on which our own research then suggests the presence of undisclosed SEC or other governmental investigation and/or law enforcement activity. This embargo on trading by our employees or principals lasts for a minimum of 5 days after the investigation's existence has been published by us; added to our database (even if not published); or our research on that issue otherwise ceases.

In addition, Disclosure Insight, Inc. prohibits its employees and principals from trading in any individual public company security (or derivative thereof), of any company about which a research report, blog entry, video, audio, or other publication has commenced. This embargo on trading by our employees lasts for a minimum of 5 days after the investigation’s existence has been published; added to our database (even if not published), or our research on that issue otherwise ceases.

On a severely limited basis, we may exercise flexibility of this embargo period if an employee is in “extreme financial hardship” as defined by the CFA Institute Code of Ethics. It's worth noting that since 2000 we have never had to revisit our rules. But being committed to transparency, it's important that we hold ourselves to the same standards we expect others to follow.

Disclosure Insight, Inc. otherwise permits, and encourages, its employees to freely trade in any securities so long as such trading is not deemed as in conflict with this policy or our subscribers. We similarly place no holding period limits or restrictions on such personal trading. This could, and often does, include trading in mutual funds, exchange traded funds (ETFs), and derivatives thereof which may include covered names as components of the overall funds and/or ETFs.

Disclosure Insight, Inc. does not engage in investment banking activities or take any security positions, except those necessary for routine corporate treasury functions

Privately-Held Company

Disclosure Insight, Inc. is a privately-held publisher of investment research that is not in any way affiliated with the U.S. Securities and Exchange Commission (“SEC”) or any other branch or agency of government. It is 100% owned by John P. Gavin, CFA.

At times Mr. Gavin may have provided business advice or made investments in the securities or investment opportunities offered by privately-held ventures. At present, none of those activities undertaken by Mr. Gavin are anticipated to involve the securities of public companies on which Probes Reporter, LLC would report. Should conflicts with this statement arise in the future they will be timely disclosed.